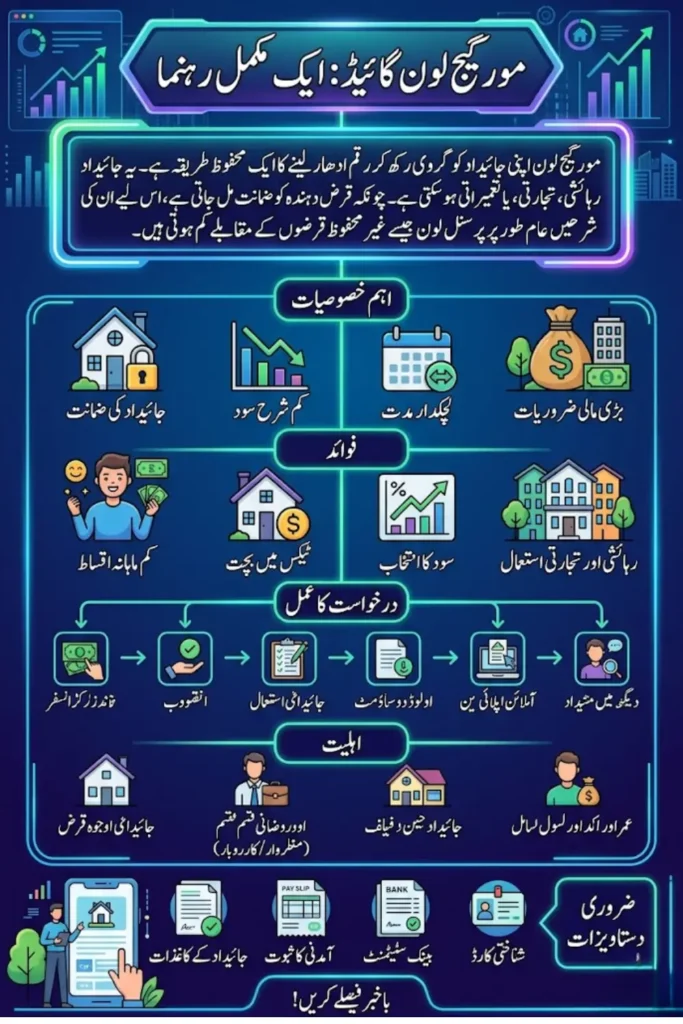

A mortgage loan is a secured way to borrow money by using your property as collateral. This property can be residential, commercial, or even under construction. Because the lender has security in the form of your asset, mortgage loans usually come with lower interest rates compared to unsecured loans like personal loans.

This type of loan is widely used for multiple financial needs, including buying a home, expanding a business, or handling large expenses. However, since your property is at stake, it is important to understand how mortgage loans work before applying.

What is a Mortgage Loan?

A mortgage loan allows you to use your owned property to get funds from a bank or financial institution. The property remains in your name, but the lender has legal rights over it until the loan is fully repaid. If repayments are not made, the lender can sell the property to recover the amount.

Because of this security, lenders consider mortgage loans low-risk and offer longer repayment periods. This makes it easier for borrowers to manage their monthly payments without financial pressure.

Key features of a mortgage loan:

- Secured against property

- Lower interest rates than unsecured loans

- Flexible repayment tenure (15–30 years)

- Suitable for large financial needs

You can also read: Complete BISP Guide for Women 2026

Home Mortgage Loan vs General Mortgage Loan

A home mortgage loan is specifically taken to purchase a house. In this case, the property being bought becomes the collateral. It is mainly used by individuals planning to own a home without paying the full price upfront.

On the other hand, a general mortgage loan (loan against property) is broader. You can use any property you already own to borrow money for different purposes such as business expansion, education, or medical needs.

Main differences:

- Home loan is for buying property

- Mortgage loan can be used for multiple purposes

- Both are secured but serve different goals

Benefits of Mortgage Loans

Mortgage loans offer several advantages that make them a preferred financing option for many individuals and businesses. The biggest benefit is affordability due to lower interest rates and longer repayment periods.

Another important advantage is tax benefits in some countries, where borrowers can reduce taxable income by claiming deductions on interest payments and principal repayment.

Key benefits include:

- Lower interest rates compared to personal loans

- Long repayment tenure reduces monthly burden

- Tax benefits on interest and principal (where applicable)

- Option to choose fixed or floating interest rates

- Flexibility to use residential or commercial property

- Continued ownership of property if repayments are made on time

Mortgage Loan Interest Rates and Charges

Interest rates on mortgage loans usually range between moderate levels compared to other loans. The exact rate depends on factors like your credit profile, income, and property value.

Apart from interest, lenders may charge additional fees. These costs can increase the total loan amount if not considered carefully. Mortgage Loan Complete Guide

| Type of Charge | Description |

|---|---|

| Interest Rate | Cost of borrowing, fixed or floating |

| Processing Fee | Charged for loan approval and paperwork |

| Documentation Charges | Cost of verifying legal documents |

| Late Payment Fee | Applied when EMI is delayed |

| Prepayment Charges | Fee for early loan repayment (if applicable) |

It is always important to compare offers from multiple lenders before finalizing a loan.

Eligibility Criteria for Mortgage Loans

Lenders evaluate several factors before approving a mortgage loan. These checks help them understand your repayment capacity and reduce their financial risk.

Your income, age, and financial stability play a major role in determining whether your application will be approved. The value and condition of the property also significantly affect the loan amount.

Common eligibility factors:

- Age and income level

- Employment type (salaried or self-employed)

- Market value of the property

- Existing loans and liabilities

- Number of dependents

You can also read: Apna Khet Apna Rozgar Scheme Apply

Documents Required for Mortgage Loan

Submitting the correct documents is a crucial step in the loan approval process. The requirements may vary depending on your employment status and the lender’s policies.

Salaried individuals usually need proof of income and bank statements, while self-employed applicants must provide financial records of their business. Mortgage Loan Complete Guide

Basic documents include:

- Identity proof (CNIC, passport, etc.)

- Address proof

- Salary slips or income proof

- Bank statements (last 6 months)

- Property ownership documents

- Financial statements (for self-employed individuals)

Step-by-Step Process to Apply for a Mortgage Loan

Applying for a mortgage loan involves several stages, from selecting a lender to receiving the final amount. Understanding the process helps avoid delays and improves approval chances.

The lender carefully verifies your financial and property details before approving the loan. Once approved, funds are released after final documentation.

Application process:

- Choose a reliable lender

- Fill out the loan application

- Submit required documents

- Property evaluation by the lender

- Eligibility and credit assessment

- Loan approval and sanction letter

- Final document verification

- Loan disbursement

Important Factors to Consider Before Applying

Before applying for a mortgage loan, you should evaluate all important aspects to avoid financial stress in the future. The loan amount, interest rate, and repayment tenure must match your financial capacity.

Ignoring hidden charges or choosing a long tenure without planning can increase the total cost of borrowing. Mortgage Loan Complete Guide

| Factor | Why It Matters |

|---|---|

| Loan Amount | Depends on property value and lender policy |

| Interest Rate | Affects total repayment cost |

| Tenure | Longer tenure reduces EMI but increases interest |

| Fees & Charges | Hidden costs can increase loan burden |

| Repayment Plan | Must align with your monthly income |

Tips to Get a Lower Interest Rate

Getting a lower interest rate can save a significant amount over the loan period. Lenders offer better rates to borrowers with strong financial profiles and good credit history.

Simple planning and smart decisions can help reduce the overall cost of your mortgage loan.

Useful tips:

- Maintain a good credit score

- Compare multiple lenders before choosing

- Avoid applying for multiple loans at once

- Choose a suitable loan tenure

- Borrow only what you can easily repay

You can also read: Apply for a Rahmat Card Easily

Conclusion

A mortgage loan is a powerful financial tool that can help you meet major expenses while keeping your monthly payments manageable. Its lower interest rates and flexible repayment options make it a practical choice for both individuals and business owners.

However, since your property is used as collateral, careful planning is essential. Always compare different loan offers, understand all terms, and ensure that repayments fit your budget. Making informed decisions will help you use a mortgage loan wisely and safely. Mortgage Loan Complete Guide